Limiting a Retirement Classic: The IRA May See Some Unwelcome Changes

- The Seven Group

- Sep 30, 2021

- 4 min read

A look inside the proposed changes to a retirement staple - the IRA - as part of the Build Back Better Act, which has ambitious goals for infrastructure and bolstering the social safety net.

IRAs were created in 1974 under the ERISA legislation that set minimum standards for company pension plans. They were conceived as a way for individuals not covered by those plans to access tax-advantaged retirement savings. They’ve changed over the decades, and usually for the better. Roth IRAs and the ability for folks who already have a 401(K) to access them are just two examples.

The proposed Build Back Better Act, which has ambitious goals for infrastructure and bolstering the social safety net, must find a way to pay for them – and is setting sights on this retirement staple. The changes may not seem to affect that many retirement savers on the surface, but as the details become clearer the impact becomes greater.

We break down the details.

An Asset Level Limit for Contributions

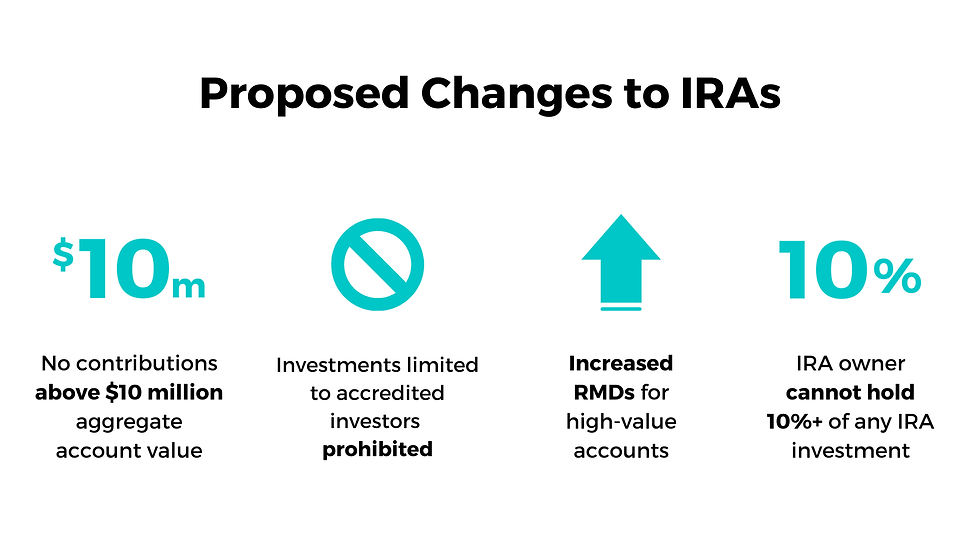

One of the legislation's goals is to reset these tax-advantaged accounts so that they primarily benefit middle-income retirement savers. The proposal is to prohibit contributions to IRA accounts if the aggregate value of all defined contribution retirement plans is above $10 million. The income limit here is the same as other provisions included in the Act: Taxable income exceeding $450,000 in the case of a married couple filing jointly or $400,000 in the case of single or married taxpayers filing separately.

The legislation proposes that all accounts be added together for the $10 million threshold figure. For example, if you have a 401(k) with your employer, and you inherited an IRA from your parents, and the total value of both those accounts combined is over $10 million, you cannot contribute to an additional IRA account in that year.

SEP or SIMPLE IRA accounts are not included in this – you are still able to make contributions to those accounts.

There are also some changes to required minimum distributions (RMDs) for high-value accounts. The new RMD would be 50% of the portion of the account over $10 million and $100% of any amount exceeding $20 million. If passed, this is effective for tax years beginning after Dec. 31, 2021.

Prohibitions on Investments

The Act would prohibit IRAs from investing in a security whose issuer requires a specified minimum of income or assets or requires specific levels of education, licensing, or credentialing. The stated purpose is to prevent IRA investments in assets that are not broadly available to the general public. However, this would have two potential impacts. Many investors seeking yield in this low-rate environment or who want access to non-correlated investments have turned to alternatives, which have become mainstream. They are, however, often still limited to accredited investors. The accredited investor standard is $200,000 in income or $1 million in assets – which many people close to or in retirement meet easily. The second potential problem is that the provision could be interpreted to apply to lower-fee share classes that are predicated on higher investment amounts, which would eliminate a way to lower fees in an investment plan.

A Source of Real Estate Funding Could Be Eliminated Currently, IRAs are not permitted to be invested in any asset where the IRA owner holds 50% or more of the entity or is an officer or director. The bill would change this to a 10% limit. This would impose significant limits on the funding of small businesses, private placements and LLC structures that make real estate investing more efficient.

The Bottom Line

Planning for tax efficiency, whether you’re retired or still working, is complex in any year. With so many changes being proposed and the pandemic's effects still being worked through, this year can potentially impact your financial plan for years to come. Taking a close look at your financial plan while there is still time to make changes can pay off.

IMPORTANT DISCLOSURES

This work is powered by Seven Group under the Terms of Service and may be a derivative of the original. More information can be found here.

The information contained herein is intended to be used for educational purposes only and is not exhaustive. Diversification and/or any strategy that may be discussed does not guarantee against investment losses but are intended to help manage risk and return. If applicable, historical discussions and/or opinions are not predictive of future events. The content is presented in good faith and has been drawn from sources believed to be reliable. The content is not intended to be legal, tax or financial advice. Please consult a legal, tax or financial professional for information specific to your individual situation.

This content not reviewed by FINRA

Basepoint Wealth, LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance.

Comments